Last Updated on July 8, 2026

APY (Annual Percentage Yield) is the real rate of return you earn on savings or investments in one year after accounting for compound interest. It shows how much your money actually grows, not just the base interest rate. Unlike simple interest, APY includes compounding, which means you earn interest on both your original deposit and the interest already earned. This makes APY a more accurate measure of earnings in banking, savings accounts, and crypto yield platforms.

When people first see the term APY, it often feels like financial jargon designed to confuse them. You open a bank app, and suddenly you see something like “4.75% APY.” At that moment, a simple question hits your mind:

What does APY mean, and how much money will I actually earn?

Here’s the simple truth.

APY (Annual Percentage Yield) tells you how much your money grows in one year when interest compounds over time.

It’s not just a number. It’s a real-world growth indicator for your savings or investment.

Think of it like this:

If interest rate is the seed, APY is the full-grown tree.

The difference is compounding. And compounding changes everything.

APY Definition: Annual Percentage Yield Meaning Explained

Let’s break the APY definition into a clean, practical explanation.

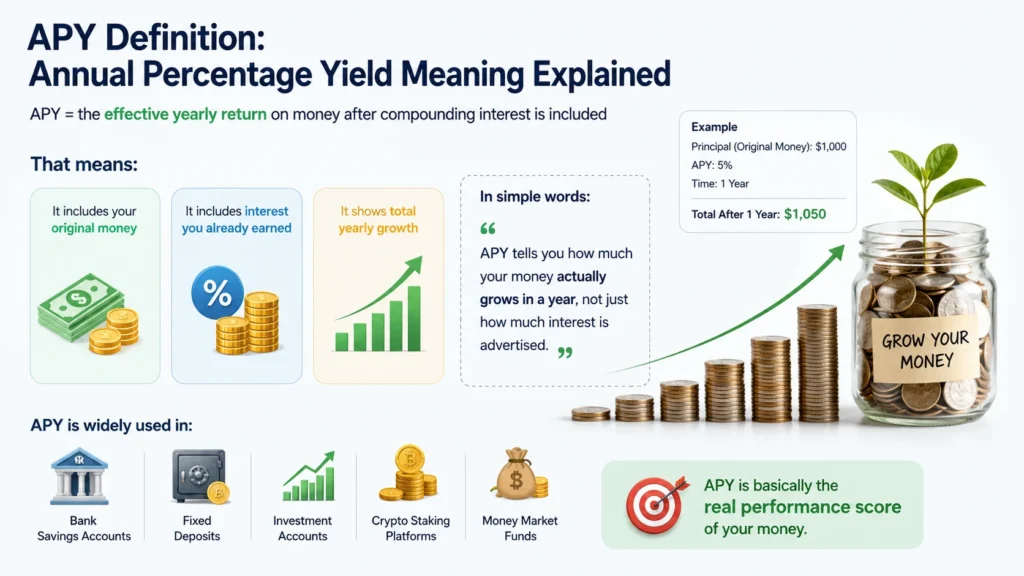

APY = the effective yearly return on money after compounding interest is included

That means:

- It includes your original money

- It includes interest you already earned

- It shows total yearly growth

In simple words:

“APY tells you how much your money actually grows in a year, not just how much interest is advertised.”

This is why APY is widely used in:

- Bank savings accounts

- Fixed deposits

- Investment accounts

- Crypto staking platforms

- Money market funds

APY is basically the real performance score of your money.

What is APY? Understanding APY Finance Meaning in Real Life

To understand what is APY, imagine two savings accounts:

- Account A offers 5% interest (simple interest)

- Account B offers 5% APY (with compounding)

At first glance, they look identical. But they are not.

Here’s what happens:

Account A pays interest only on your original deposit.

Account B pays interest on your deposit and on previous interest.

That difference creates a gap that grows bigger over time.

For example:

| Year | Simple Interest | APY (Compounding) |

| 1 | $50 | $50 |

| 2 | $100 | $102.50 |

| 3 | $150 | $157.62 |

| 5 | $250 | $276.28 |

That small difference looks harmless in year one.

But over time, it snowballs.

This is the hidden power behind APY finance meaning.

How APY Works: The Role of Compound Interest

Now let’s get into the engine behind APY: compound interest.

APY works because of a simple idea:

You earn interest on interest.

This is where money starts behaving like a snowball rolling downhill. It starts small. Then it grows faster and faster.

Interest Compounding Explained

Compounding can happen in different ways:

- Daily compounding

- Monthly compounding

- Quarterly compounding

- Annual compounding

The more frequent the compounding, the higher your APY becomes.

Even if two accounts show the same interest rate, their APY can differ based on compounding frequency.

Simple Analogy

Imagine you plant a mango tree.

- Simple interest is like only collecting fruit from the main tree

- Compound interest is like planting new trees from every fruit you pick

Soon, you don’t have one tree. You have a whole orchard.

That’s how APY grows money.

APY Formula Explained (Without Complexity Overload)

The APY formula looks like this:

APY = (1 + r/n)ⁿ − 1

Let’s simplify it.

- r = interest rate

- n = number of compounding periods per year

Now forget the math for a moment.

What this formula actually does is:

It calculates how much your money grows when interest keeps adding itself again and again.

Example Breakdown

Let’s say:

- Interest rate = 5%

- Compounded monthly

Even though the rate is 5%, APY becomes slightly higher:

- APY ≈ 5.12%

That extra 0.12% comes from compounding.

It looks small. But on large savings, it matters a lot.

APY vs APR: The Most Important Financial Difference

People often confuse APY vs APR difference, but they are not the same.

Here’s the simplest breakdown:

- APY = what you earn

- APR = what you pay (usually on loans)

Clear Comparison Table

| Feature | APY | APR |

| Meaning | Annual Percentage Yield | Annual Percentage Rate |

| Includes compounding | Yes | No |

| Used for savings | Yes | Rarely |

| Used for loans | No | Yes |

| Shows real return | Yes | Not fully |

Real-Life Impact

Let’s say you take a loan:

- APR is 10%

- But interest compounds monthly

You will actually pay more than 10% over time.

That’s why lenders show APR, but your real cost behaves closer to APY-style growth.

Where APY is Used in Banking and Finance

You see APY in banking almost everywhere where money grows.

Common APY-Based Products

- Savings accounts

- High-yield savings accounts

- Fixed deposits (FDs)

- Money market accounts

- Retirement accounts

Modern Finance Uses

APY is not just old-school banking anymore. It’s also used in:

- Crypto staking rewards

- DeFi lending platforms

- Yield farming systems

- Investment apps offering passive income

Why Banks Show APY Instead of Interest Rate

Because APY gives a clearer picture.

It answers the real question:

“How much money will I actually earn in a year?”

Not just:

“What is the base rate?”

Why APY Matters for Your Financial Growth

Understanding APY interest rate meaning can completely change how you manage money.

Here’s why it matters:

It helps you compare accounts fairly

A 4% APY account may outperform a 4.2% simple interest account.

It shows real earnings

You don’t get misleading numbers. You see actual growth.

It protects you from hidden differences

Two accounts can look similar but behave differently due to compounding.

It improves long-term wealth building

Even a 1% difference in APY can create thousands over years.

Real Example

If you invest $10,000:

- At 4% APY → ~$10,480 after 1 year

- At 5% APY → ~$10,512 after compounding differences

Now stretch that over 10 years, and the gap becomes massive.

Common Misunderstandings About APY

Many people misunderstand APY meaning. Let’s clear that up.

“APY is just interest rate”

Wrong. APY includes compounding. Interest rate alone does not.

“Higher APY always means better investment”

Not true. Risk matters too. Crypto APY can be high but unstable.

“APY guarantees profit”

False. Variable accounts can change anytime.

“APY is the same everywhere”

No. It changes based on:

- Institution

- Compounding frequency

- Market conditions

Factors That Affect APY

Several things influence your final APY:

- Compounding frequency

- Base interest rate

- Bank or platform policy

- Market conditions

- Promotional offers

Even small changes in compounding frequency can shift returns noticeably.

How to Calculate Earnings Using APY (Simple Example)

Let’s say you invest:

- $1,000

- APY = 5%

- Time = 1 year

You earn:

- $1,050 total (approx.)

Now compare:

- 3% APY → $1,030

- 6% APY → $1,060

That difference scales fast with bigger money.

APY in Banking vs Crypto: Modern Comparison

APY is now used outside banks too.

Banking APY

- Stable

- Predictable

- Low risk

- Lower returns

Crypto APY

- High returns (sometimes 5%–20%+)

- High volatility

- Risk of platform failure or price swings

Simple Reality Check

Higher APY usually means higher risk.

No free lunch exists in finance.

How to Compare APY Like a Smart Investor

Don’t just chase the biggest number.

Look deeper:

- Is APY fixed or variable?

- How often does it compound?

- Are there withdrawal limits?

- Are there hidden fees?

- What’s the risk level?

Smart money decisions come from context, not just percentages.

Tips to Maximize Your APY Benefits

If you want to get more from APY:

- Choose accounts with daily or monthly compounding

- Reinvest your earnings instead of withdrawing early

- Compare multiple banks before locking money

- Avoid low APY accounts that lose value to inflation

- Balance risk and reward carefully

Final Takeaway

At its core, APY meaning is simple:

It tells you how fast your money grows over time with compounding included.

But the deeper truth is more powerful.

APY is not just a number.

It’s a reflection of financial time working in your favor.

Small differences today can become massive differences tomorrow.

That’s the real power behind APY.

Michael Anderson is a content writer specializing in word meanings, definitions and clear explanations of modern terms and phrases.